By Vaishnavi Kumari

“If the 20th century ran on oil and steel, the 21st century runs on compute and the minerals that feed it.” This was said by the Under Secretary of Economic Affairs, Jacob Helberg (U.S. Dept. of State). In the 21st century, the quest for international domination in the arena of technological advancement has led to a race between two powerful giants of global politics, the US and China, to secure strategic leverage over Rare Earth Elements (REEs). REEs have become a central coliseum of US-China strategic rivalry, with China's supremacy over the entire production cycle providing substantial economic and military leverage against the US (Konyshev, 2026). Rare-earth elements (REEs) are a set of 17 elements that are essential components of various high-tech products, consumer electronics, green economy technologies, and defense systems (Pawar and Ewing, 2022; Balaram, 2019). The US-China rare earth conflict is dramatically redrawing geopolitical alignments, supply chain architectures, and security ties across the Indo-Pacific.

Rare Earth Landscape and China’s Weaponisation of REEs:

REEs are elements that have become immensely essential in the modern age of technology due to their distinctive magnetic, phosphorescent, and catalytic capabilities (Balaram, 2019). These elements are rapidly utilized for numerous purposes. These elements are referred to as “The Vitamins of Modern Industry” because of their importance in technologically advanced equipment (Faccioli, 2016).

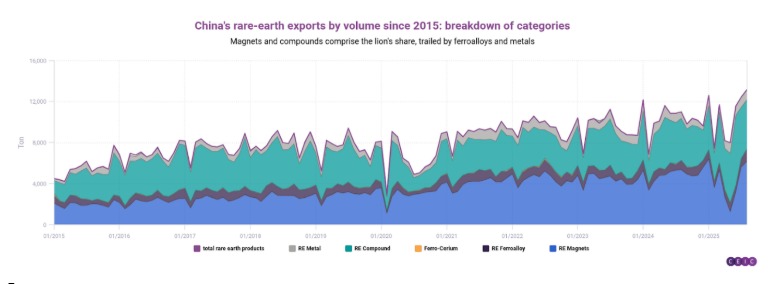

Rare earths are not inherently rare; they are found all over the world. Despite this global presence, the rare earth supply chain has grown significantly, with China dominating the processing stages, accounting for over 90% of global processing (International Energy Agency, 2025). China’s rare earth output has increased dramatically, while its competitors, notably the United States, Australia, and Russia, lag far behind. According to USGS data, China’s production of rare earth oxides (REO) has increased from less than 50,000 tons in the mid-1990s to 270,000 tons in 2024, accounting for over 70% of the global output.

China’s vast reserves and years of technological know-how are the primary reasons for its unwavering dominance in the global rare earth market. China’s near-monopoly on REEs enables it to exert price control, manage supply chains, and apply geopolitical pressure, rendering many REE-dependent countries vulnerable to Chinese influence (Chaudhuri, 2025). China’s dominance in the rare earth business now allows it to influence global production, trade discussions, and tariffs, all of which affect rare earth-dependent industries.

Washington’s Response and the Broader Strategic Reordering

Last year, in reaction to Trump's ‘Liberation Day’ tariffs, China imposed limits on a dozen rare earths exported to the United States, which were then expanded to include any ‘parts, components, and assemblies’ utilizing Chinese rare earth elements or manufactured with Chinese critical minerals technologies. Even after the US stock markets fell and the Trump administration reduced tariffs, China maintained some of its regulations. Since then, Trump’s rhetoric toward China has become more reserved. Beijing has also hampered Western efforts to diversify supply chains through ‘predatory pricing.’ In 2024, Chinese exports ascended even faster, bringing prices down by 80% and forcing projects in the United States, Canada, and Australia to close (Fernandez, 2026).

To counter this vulnerability, the US administration harnessed two competitive advantages: the private sector and multilateral cooperation with allies. Under multilateral cooperation, the Minerals Security Partnership (MSP) was established in 2022, bringing together 14 countries and the European Union, which account for more than half of the global GDP and 60% of mineral demand. Its early members included Australia, Germany, France, India, the United Kingdom, Canada, Japan, and South Korea. Additionally, under the Trump administration, the US launched the Pax Silica Initiative in December 2025, which aims to develop a safe, affluent, and innovation-driven silicon supply chain from crucial minerals and energy inputs to sophisticated manufacturing, chips, AI infrastructure, and logistics. Pax Silica, which is based on close liaison with credible partners, seeks to lessen coercive reliance, safeguard the resources and skills essential to artificial intelligence, and guarantee that aligned countries can create and implement advanced technologies globally.

The United States’ supervision of the liberal Indo-Pacific order invites serious scholarly scrutiny. While Washington champions “Free and Open Indo-Pacific” principles, its contemporary embrace of bilateralism, mercantilist friend-shoring, and the weaponisation of rare earth access through basing rights and conditions reveal a structurally inconsistent hegemon, one that revises the rules it professes to uphold whenever systemic competition intensifies (Sato, 2023). The emerging bifurcation of global mineral supply chains into rival blocs threatens to institutionalize what might be termed a resource “iron curtain”, less a product of multipolar anarchy than of Washington's own selective multilateralism. If the post-war order's legitimacy rested on consent manufactured through inclusive rule-making, today’s defence-industrial decoupling and ally shoring arrangements increasingly replace transactional coercion for that consent (Sato, 2023). The historical precedent that both Japan’s inclusion and China’s exclusion were imposed, not negotiated, suggests that American order-building has always been constitutively coercive; what is novel is the diminishing ideological coherence with which this coercion is now exercised.

Conclusion

The rare earth rivalry between Washington and Beijing is far more than just a trade dispute. China’s overwhelming monopoly across the rare earth supply chain, especially in the upstream and midstream segments of the mineral ecosystem, has provided it with strategic leverage, which it has weaponised. In response, the US has pursued multilateral frameworks and the strategy of ‘friendshoring’ and coupled it with allied supply chain diversification. However, these efforts remain nascent and are fragmented. The growing divergence of global mineral supply chains into competing blocs risks deepening geopolitical instability and economic vulnerability in dependent nations. Therefore, it has become imperative for nations to build a resilient and secure rare earth supply chain that is independent of China, making it an economic priority and thus vital for national energy security. How efficiently the United States and its partners respond to China's current structural dominance will mainly determine the balance of technological power in decades ahead.

Vaishnavi Kumari is a postgraduate in Political Science from Banaras Hindu University. The views expressed in the above piece are personal and solely those of the author. They do not necessarily reflect the views of Kalinga Institute of Indo-Pacific Studies.

Image Source: CEIC

KIIPS is a premiere think-tank that intends to provide a platform to academics, researchers, scholars and experts from across the country and abroad.